Table of Contents

Definition of Accounting

Accounting is the process of the systematic recording, summarizing, analyzing, and reporting of a business’s financial transactions. It is not only necessary for decision-making, but also legal to comply with the laws.

Objectives of Accounting

- Recording Transactions: Recording of transactions in chronological order.

- Profit check — Financial statements to assess business performance

- Analyzing Financial Position: Creating a balance sheet to assess assets, liabilities, and equity

- Disseminating the Information: Enabling management, investors, and regulators to make informed decisions.

- Compliance and Accountability: Making sure laws and standards such as GAAP are followed.

Importance of Accounting

- Assists in Decision-Making: Presents a clear view of financial status, which is crucial for making strategic decisions.

- Legal Compliance: Helps in return of filing tax returns, GST filing, & reporting.

- Financial Control: Monitoring revenue and expenditures to avoid fraud and abuse of resources.

- Business Valuation: Provides data needed to value a business in mergers, acquisitions, or investments.

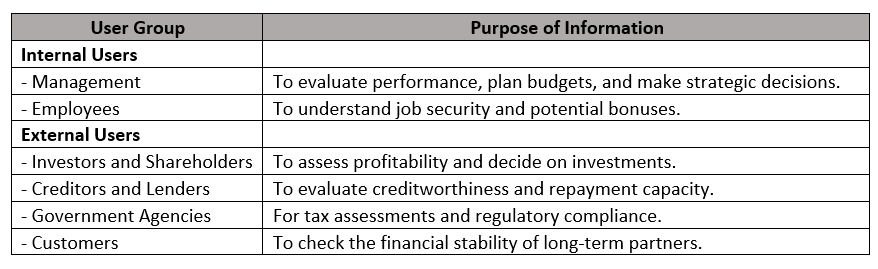

Users of Accounting Information

Accounting Principles

1. Generally Accepted Accounting Principles (GAAP)

Set of standards in financial reporting guidelines to provide consistency, transparency, and comparability.

2. Accrual Concept

Revenue and expenses are recorded when earned or incurred, not when cash is received or paid.

For Example: Recording a sale when you issue an invoice and not when you receive the payment

3. Going Concern Concept

Assumes the continuation of the operation of the business into the foreseeable future.

For example, Assets are appraised and filed based on their utilities rather than their liquidation value.

Types of Accounts and Rules

Accounting is the classification of accounts into 3 categories and each category has its own set of rules called the Golden Rules of Accounting. Let’s discuss these points in detail:

1. Personal Accounts

Definition:

These accounts relate to individuals, organizations, or entities with which the business has direct dealings. Personal accounts can be further categorized as:

- Natural Persons: Individuals (e.g., Aman’s Account).

- Artificial Persons: Organizations or companies (e.g., XYZ Ltd.).

- Representative Personal Accounts: Accounts representing groups of people or amounts owed/receivable (e.g., Outstanding Rent Account, Prepaid Insurance Account).

Golden Rule:

- Debit the Receiver

- Credit the Giver

Example:

- Transaction: Paid ₹10,000 to Aman.

Entry:- Debit: Aman’s Account (Receiver) ₹10,000

- Credit: Cash Account (Giver) ₹10,000

- Transaction: Received ₹5,000 from XYZ Ltd.

Entry:- Debit: Cash Account (Receiver) ₹5,000

- Credit: XYZ Ltd. Account (Giver) ₹5,000

2. Real Accounts

Definition:

These accounts relate to the physical and the non-physical assets of the company. Even if the business ceases to be, they persist. Examples are Machinery, Furniture, Buildings, Patents and Trademarks.

Golden Rule:

- Debit What Comes In

- Credit What Goes Out

Example:

- Transaction: Purchased machinery for ₹50,000.

Entry:- Debit: Machinery Account (What Comes In) ₹50,000

- Credit: Cash Account (What Goes Out) ₹50,000

- Transaction: Sold furniture for ₹20,000.

Entry:- Debit: Cash Account (What Comes In) ₹20,000

- Credit: Furniture Account (What Goes Out) ₹20,000

3. Nominal Accounts

Definition:

The accounts deal with expenditure loss, income, and gains. They do not indicate any physical asset to receive but help calculate the profit or loss of the business.

Golden Rule:

- Debit All Expenses and Losses

- Credit All Incomes and Gains

Example:

- Transaction: Paid salary of ₹15,000.

Entry:- Debit: Salary Account (Expense) ₹15,000

- Credit: Cash Account ₹15,000

- Transaction: Earned commission of ₹10,000.

Entry:- Debit: Cash Account ₹10,000

- Credit: Commission Account (Income) ₹10,000

Summary of Golden Rules

Sahab Academy is the source of this YouTube video.