One of the most important financial reports for businesses is the profit and loss statement (P&L statement), also referred to as an income statement. It details revenues, costs, and expenses over a particular timeframe, usually quarterly or yearly. This statement makes awareness of the profitability of a business and assists stakeholders in making knowledgeable decisions.

Table of Contents

This article will walk you through the process, step by step, to prepare a clear and accurate P&L statement.

Components of a Profit and Loss Statement

Before we start talking about the preparation process, let’s understand the important elements of the P&L statement:

Revenue (Sales)

- All income earned from the sale of goods or services falls under this category.

- By definition, it is important to separate operating revenue (core business activities) versus non-operating revenue (i.e., interest income or proceeds of asset sales).

Cost of Goods Sold (COGS)

- Direct costs of production of goods/services sold in the period

- These include Direct materials, Direct labor, and manufacturing overheads

Gross Profit

- Calculation of Gross profit: Gross Profit = Revenue – COGS

- It shows profit from ongoing business before subtracting other expenses.

Operating Expenses

- These are the business operating costs, other than COGS.

- Salary, rent, utility, marketing expenses, etc.

Operating Profit (EBIT)

- Also referred to as Earnings Before Interest and Taxes (EBIT); computed as: Operating Income = Gross Income – Operating Expenses

Other Income and Expenses

- Below the Other Income, there are non-operational items like interest income, interest expenses, or capital gains/losses.

Net Profit

- Net profit, which is the bottom line of the P&L statement, is computed as: Net Profit = Operating Profit + Other Income – Other Expenses

- It indicates the net gains of the business.

9 Steps to Prepare a Profit and Loss (P&L) Statement

Step 1: Select the Reporting Period

- Decide the particular duration you owe to compile the statement (e.g., monthly, quarterly, or annual).

- Compare similar periods to make meaningful comparisons between repeated periods.

Step 2: Gather Financial Data

- Gather all pertinent information — sales records, invoices, receipts, expense reports, and so forth.

- All transactions are recorded and categorized correctly in your accounting system.

Step 3: Total revenue calculation

- Total all income from sales/services received in the reporting period.

- Lastly, put your other income with separate what comes of rental, dividends, or interest earnings.

Step 4: Calculate the Cost of Goods Sold (COGS)

- Cost of Goods Sold – Find the total expense directly associated with the production/purchase of goods and/or services sold

- Apply this COGS equation: COGS = Beginning Inventory + Purchases – Ending Inventory

Step 5: Compute Gross Profit

- Calculate gross profit by subtracting COGS from the total revenue.

- Shows the efficiency of production or service delivery processes by way of gross profit

Step 6: Journal Operating Expenses

- Include all operating costs, like salaries, utilities, depreciation, and marketing expenses.

- Keep it organized, so keep your expenses well-categorized.

Step 7: Calculate Operating Profit (EBIT)

- Subtract total operating expenses from gross profit to calculate the operating profit.

- This measure is used to evaluate how profitable a firm’s core operations are.

Step 8: Add any Other Income and Expenses

- Include any non-operating income (interest earned or investments sold at a profit, for example).

- Deduct any non-operating costs (like loan interest or losses on asset sales).

Step 9: Compute Net Profit

- Net profit is obtained by adding other income to the operating profit and deducting other expenses.

- Net profit is the overall profitability of the business after accounting for all proceeds and overhead.

Tips for Accurate P&L Statement Preparation

Use Accounting Software

- Modern accounting tools such as QuickBooks, Tally, or Zoho Books automate and simplify the process minimizing the scope of error.

Maintain Accurate Records

- Maintain meticulous records of all financial transactions for audit purposes.

Adopt a Consistent Format

- Prepare your P&L statement using a standardized template or chart of accounts which you can replicate in future periods.

Reconcile Accounts Regularly

- By regularly reconciling the bank statements and other accounts, discrepancies can be easily identified.

Review and Analyze Trends

- Looking at P&L statements over different periods for trend analysis and improvement opportunities.

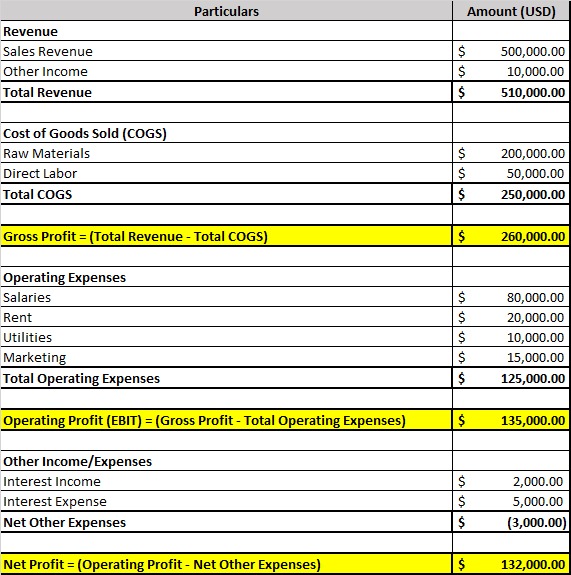

Example: Profit and Loss Statement

Here’s a basic illustration of a P&L statement for a sample company:

Aman Enterprise

Profit and Loss Statement

For the Year Ended December 31, 2024

Importance of a P&L Statement

Performance Measurement

- It is used for assessing the profitability and operational aspects of the business.

Decision-Making Tool

- Useful for budgeting, cost control, and resource allocation.

Compliance and Reporting

- P&L statement is commonly needed for tax filing and investor reporting.

Attracting Investors

- A comprehensive P&L statement communicates financial health and transparency to prospective investors.

Conclusion

A profit and loss statement is an important financial document that gives a clear perspective of a business’s profitability. However, by breaking it down into key elements and following the simple steps above, a P&L statement can be thorough, informative, and accurate. Whether you’re an accounting professional, small business owner, or working a regular job, mastering this process is vital to success.

Get your financial data organized today, and start taking control of your business’s finances!

Frequently Asked Questions (FAQs)

Q1: What is a profit and loss (P&L) statement?

Ans: A profit and loss statement is a financial document that summarizes a company’s revenues, costs, and expenses over a specific period, usually a fiscal quarter or year.

Q2: Why is a P&L statement important?

Ans: A P&L statement is crucial for understanding a company’s financial performance, profitability, and ability to generate revenue over time.

Q3: What are the main components of a P&L statement?

Ans: The main components include revenue, cost of goods sold (COGS), gross profit, operating expenses, and net income or loss.

Q4: How often should I prepare a P&L statement?

Most businesses prepare P&L statements monthly, quarterly, and annually to track financial performance regularly.

Q5: What’s the difference between revenue and profit on a P&L statement?

Revenue is the total amount of money earned from sales, while profit is the amount left after subtracting all expenses from revenue.